HDFC Bank has long been the largest credit card issuer in India and one of the pioneers in developing HNI credit card products. They also became the largest credit card issuer in India and have maintained their position for a very long time. But there has been a strategic shift in the market over time (since 2020 – 21), one in which people began accumulating credit cards without using them. HDFC Bank was running with its hands tied at the time due to an RBI ban on issuing new cards.

Since then, the market evolved, with Axis Bank stepping up and withdrawing, and Citibank withdrawing from the Indian market altogether after selling its retail business to Axis Bank. ICICI Bank considered how it might be left out, so it launched Emeralde Private Metal. HSBC, one of the few foreign banks in India, is trying to replace Citi as the preferred choice (and has created a resurgence in its credit cards and HNI business like never before).

In all of this, HDFC Bank went through the motions as a consistent card issuer and a top choice for everyone. The bank has also kept the Infinia as an invite-only card, meaning the Bank gets to decide whether you get it. But in exchange, there has been consistency in the product and no knee-jerk course corrections.

HDFC Bank gives heads up on new criteria for Infinia retention

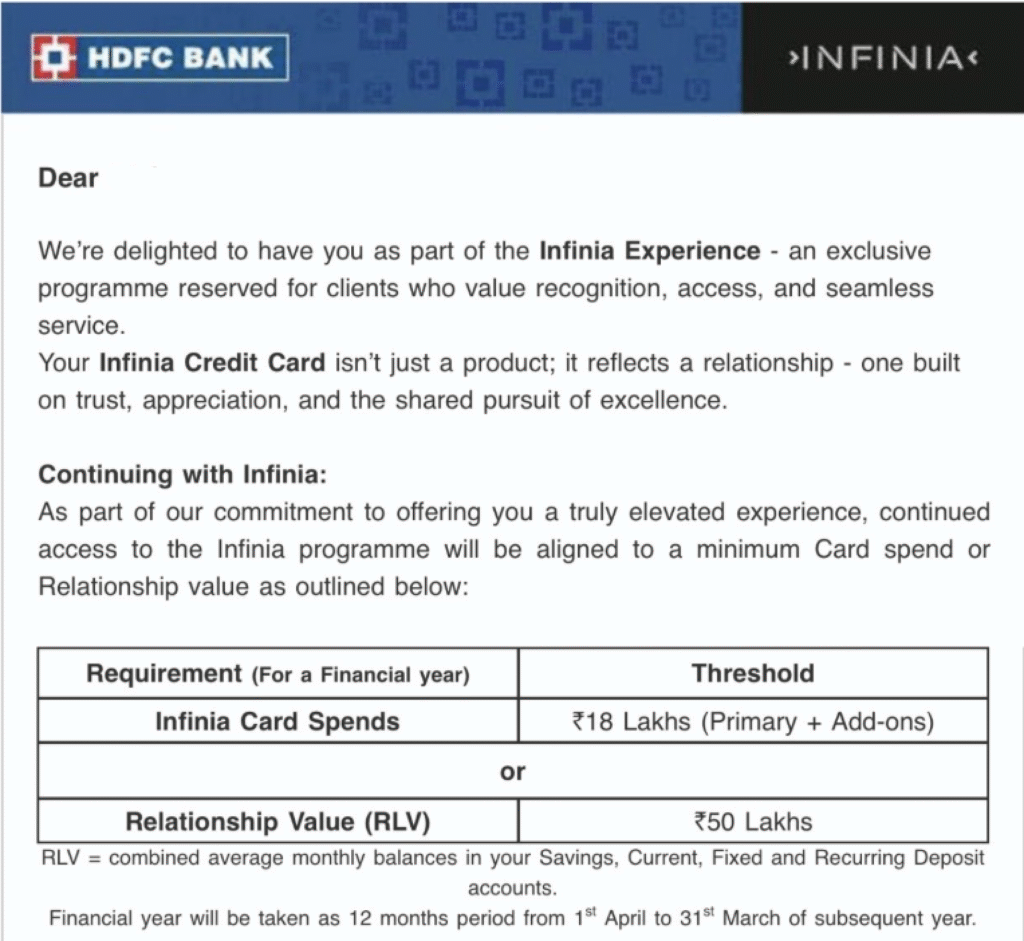

HDFC Bank has rolled out a new notice, which has been in the whispers for a few months. Infinia is moving from an invite-only programme to also anchor existing cardmembers to a minimum spend per annum or a minimum relationship value with the bank.

The Bank will measure the retention criteria for the Infinia customers as one of the two:

- Infinia Card Spends of INR 18,00,000 during April 1, 2026, to March 31, 2027

- or, Relationship Value (including Savings, Current and Term/Recurring Deposits) for INR 50,00,000 during April 1, 2026, to March 31, 2027.

Customers of the card have a year to meet the required spend or Relationship value with the Bank, and the Bank will intimate non-compliant customers in 2027.

This is not a devaluation

Customers of the Bank pay a fee for the product every year, but unfortunately, that is not enough to keep the card operational and deliver an excellent experience. A lot of that money is already being rerouted back to the customer in the form of reward points (which actually cost a lot more if you transfer them out rather than use them at the Bank’s SmartBuy website, where they’re worth INR 1). But the Bank, by using this new criterion, is taking a middle way between the Axis Bank Magnus (INR 30 Lakh NRV) and the HSBC Premier route (INR 50 Lakh NRV) for giving their card away (Total Relationship Value) and actual spends on the card. Which I feel is fair game to weed out the people who got taken away by the other alternatives in the market, and not doing their fair share of dues on the HDFC Bank Infinia.

Social Media and the public at large feel that ‘devaluation’ is the appropriate term when they don’t see changes they like. But the intent here is simple: to make the card see hands and wallets that are deserving. The expenses on a portfolio of cards, and the profits, are not financed by the annual membership fee, but by continuous usage and MDR (the fee the bank receives when you swipe the card). This is why banks are weeding out lifetime free cards, and in the case of HDFC Bank, people who the Bank thinks are unable to spend a minimum amount on Infinia.

Infinia has had all sorts of users hack their way onto the card. There are those who keep it just for the status of being exclusive. There are those who keep it for Gyftr or other categories that earn accelerated spend, and those who keep it for unlimited lounge access. Needless to say, if you were a product manager, you’d be tearing your hair out trying to keep this exclusive club of cardmembers afloat and make sure it doesn’t become a loss leader. Which is where American Express and HDFC Bank are similar in their thinking: weed out and discourage people who don’t justify having the card.

And if you are begrudging that, why are you on the firing line? Then remember, the bank could have just diluted rewards for all, but they are going the way of being unpopular with some bargain hunters to keep their equity with the real cardholders who keep the portfolio and the lights on, on the Infinia team.

Honestly, no one has taken this strategy before, and I am sure other banks will be watching the pioneering stance of HDFC Bank to see if they should follow or not.

Bottomline

HDFC Bank Credit Cards has just notified customers of its HDFC Bank Infinia, which will set a new relationship benchmark and take effect in the next financial year (April 2026 – March 2027). Those who don’t keep up will be trimmed out of the portfolio in 2027 or downgraded to another credit card in the portfolio. The mandate is to either spend INR 18 Lakhs on the card in a year, or keep INR 50 Lakhs in terms of deposits with the Bank.

What do you think of the HDFC Bank Credit Cards requirements on the Infinia?

Liked our articles and our efforts? Please pay an amount you are comfortable with; an amount you believe is the fair price for the content you have consumed. Please enter an amount in the box below and click on the button to pay; you can use Netbanking, Debit/Credit Cards, UPI, QR codes, or any Wallet to pay. Every contribution helps cover the cost of the content generated for your benefit.

(Important: to receive confirmation and details of your transaction, please enter a valid email address in the pop-up form that will appear after you click the ‘Pay Now’ button. For international transactions, use Paypal to process the transaction.)

We are not putting our articles behind any paywall where you are asked to pay before you read an article. We are asking you to pay after you have read the article if you are satisfied with the quality and our efforts.

When business butchers product because marketing went overboard with promos for rapid growth.

They added another criteria for me. For March and April 2026

As a special consideration for this year, you may continue enjoying uninterrupted access to Infinia Card by meeting either one of the following between 01st Mar, 2026 and 30th April, 2026.

Of spending 3 lakh or 30 lakh Relationship value

This is bizarre. Expecting me to spend 3 lakhs or move large amounts to HDFC at such short notice

The 1 year retention has been given to select few customers only. For others, they must complete the 18 lacs spend by April 2026 to continue enjoying the card (with some concessions).

I have a feeling that HDFC Bank is going to be very surprised. From giving away LTF Infinia upgrades during covid to now this they have proved that they are just fair weather friends. Nothing wrong with that. A smart competition PM will milk this sooner than later.

For me value of card is value of rewards over value of cost. Cost is opportunity cost from next best option. In this case, putting 50L in Saving/FD with HDFC vs say debt-mutual fund or another bank giving higher FD rate is my opportunity cost. When cost goes up without rewards going up, it is devaluation. Bank has to make money and all that alright but from customer perspective attractiveness of card has gone down and that’s fact and very much devaluation.

Well articulated and agree. This card has been on my radar for years but I never really opted, primarily because I find it poor value for money versus Axis M4B that gives better base rewards and accelerated points after crossing spend thresholds. I even took a times black which offered benefits that handsomely covered costs, but I can’t somehow justify to myself paying for Infinia, particularly after this devaluation!

M4B is a gamble. Axis is known to change rules overnight. And with the transfer restrictions on group A, M4B isn’t even a great card beyond 20-25L/year spend. What do you do with all the points if you can’t transfer them out. Not to mention if you spend large amounts, Axis will come knocking on your door for invoice copies and receipt proof. The only good card with Axis is the Olympus with a decent transfer limit of 6L points in group A category. But I trust Axis to destroy this card as well soon. Will take Infinia anytime over M4B especially if you are spending heavily on smartbuy tickets.

You can spend 18L/year on the card and not have to maintain 50L FD with the bank. I mean a genuine user of this card won’t find it that difficult to spend 18 lacs. Most folks are anyway spending 10L for fee waiver.

I haven’t received this communication from HDFC bank, probably because I’ve already crossed the threshold spend this financial year. Does that mean this spend requirement for next year isn’t applicable to me as I met the requirement this year?