American Express has launched a new promotion to promote everyday spending on the American Express Platinum Card. This promotion is the third after American Express ran similar offers in May 2020 and October 2020 for their Platinum and Centurion Cardmembers. Here are all the details about the new Amex Platinum Cashback Offer, in case you were not targetted the last time around or were not an American Express Platinum Charge Cardmember then.

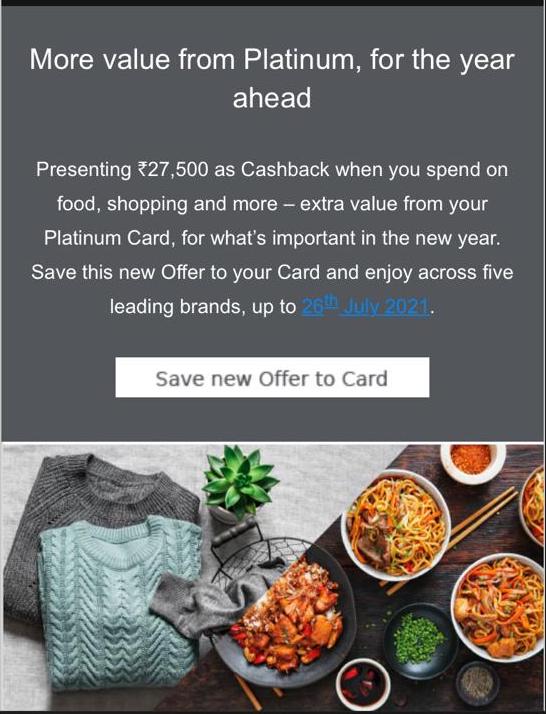

Get up to INR 27,500 cashback with More Value on Platinum offer.

The new promotion offers a 100% cash back for online & offline spends between January 27 and July 26, 2021. This offer is open for Platinum cardmembers for cards issued in India, and the maximum cap on the cashback is INR 27,500 through the promotion period. Payment needs to be made in Indian currency and is valid for purchases at the following e-retailers online or in-app or offline (at participating outlets). Excludes Flipkart payments made on delivery.

- Flipkart.com (Online/App)

- Croma.com (Online/Offline)

- Zomato.com (Online/App)

- BigBasket.com (Online/App)

- Ethoswatches.com (Online/Offline)

The list of stores where the offer is valid is here.

This offer is open only for cardholders who have been targetted for the offer. To check your eligibility for this offer, cardholders must log in to their American Express online account, check under their Amex Offers and then save the offer on their card. There is no minimum spending amount, and 100% cashback will be applied every time until the INR 27,500 limit is reached. The reimbursement should reflect in your billing statement within five working days. I have received this offer on my Platinum Charge Card. Additionally, a lot of Platinum cardmembers haven’t yet received an email from Amex, but the offer is showing up in their account.

For Centurion Cardmembers, who are an exclusive lot, the same offer exists but they get the ability to consume up to INR 55,000 worth of products from the same brands and receive a cashback for those.

If you don’t have the American Express Platinum Card, maybe it is a good idea to apply now as you would perhaps still get the offer and a lot of time to use it if you get your card soon. With our offer, you get a 110,000 Membership Reward Points on completing a minimum spend, and by January 28, 2021, also an Amazon voucher. Including this offer, I already foresee that INR 30,500 has been received as cash back from American Express with the earlier two cashback offers, and another INR 27,500 with this one will mean we have INR 58,000 back in the pocket. This excludes all the Membership Rewards promotions and all the other offers such as the App Store Cashback and the Shop Small Cashback promotions.

Bottomline

This is an excellent promotion from American Express, where they are just not rewarding cardholders for high-value purchases but also allowing earning cashback on everyday grocery and essential spends. Coupled with last offer, it just goes on to prove that American Express is trying to give as much value to their members while they are not travelling much and staying at home as well.

Have you received this new Amex Platinum Cashback offer? What is on your wish list for spending and redeeming this cashback offer?

Liked our articles and our efforts? Please pay an amount you are comfortable with; an amount you believe is the fair price for the content you have consumed. Please enter an amount in the box below and click on the button to pay; you can use Netbanking, Debit/Credit Cards, UPI, QR codes, or any Wallet to pay. Every contribution helps cover the cost of the content generated for your benefit.

(Important: to receive confirmation and details of your transaction, please enter a valid email address in the pop-up form that will appear after you click the ‘Pay Now’ button. For international transactions, use Paypal to process the transaction.)

We are not putting our articles behind any paywall where you are asked to pay before you read an article. We are asking you to pay after you have read the article if you are satisfied with the quality and our efforts.

Does anyone know about the theft/accidental purchase protection offered with AmEx cards ? I can’t seem to find the details and full t&C anywhere. Also, nothing is mentioned in product MITC’s

https://www.americanexpress.com/in/security/how-amex-protects-you/purchase-protection/

Hi ! For Plat Charge card, it can be found under:

World Class Services >Platinum Protection> Purchase Protection via https://www.americanexpress.com/in/benefits/the-platinum-card/

You can always call and check on complete deets for the same 🙂

If I use rewards multiplier to buy from Flipkart, will I get 5x points and cash back as well?

Yes, you can double dip. I did both times last year & got cashback & 5x RP as well.

Good offer for customers, the only reason for people to hold on. But a terrible failure for the company. Covid has really hit them badly.

If AmEx has to handout CASH to customers, it simply means they’re going DESPERATE. There’s a reason why in spite of their hype, they’re in a bad soup in India.

With the shaggiest customer support in the business today (done 2 nodal office and 1 ombudsman escalation in last 6 months myself for MRCC, no single query responded correctly by level 1), i suspect they must have realized that things aren’t going well for them with their spend numbers. The various fees and MDR across corporate/retail customers are their bread & butter.

When they can’t fix their merchant acceptance (when Diners is killing it with the same MDR), and their management refusing to acknowledge or act such issues (personally wrote multiple mails – even all of the small shop merchants i visited first REFUSED AmEx, and later agreed only on paying 5% extra)..

That’s interesting to hear. I’m surprised at the customer support concern. My experience on customer support has been the complete opposite -it’s been pretty great and I haven’t yet seen such levels of support on the other cards I have.

Agree on the customer support. Never faced issues. They always go over and beyond.

Agree as well, Amex CS always goes out of the way to resolve issues and is the only reason for me to hold Amex Platinum. The DCB CS is exactly opposite.

@Tanmay : Unfortunately MRCC support is horrid. It can only DREAM of coming close to Infinia/DCB support. They are so incompetent that they can’t even read the t&C on their website and interpret what it says (that was my last escalation).

In June 2020, i had to escalate that their EXECUTIVE SUPPORT rep Bavleen did not READ my complaint email regarding merchant denial of AmEx, and asked me to ‘raise it with merchant’ to accept, clearly REFUSING any ownership.

On more escalations, it turned out that their online payment gateway page is officially supported on Google Chrome / Chromium based browsers, and “may not work” on other browsers (and this was shocking for me).

Just escalated another issue to Nodal office, since nobody down below responded.

Here’s a fact. Emails to ALL escalation offices are responded by head customer services

Escalation offices :

1) Manager customer services,

2) head customer services

3) Nodal office

Looks like they are having a severe cost cutting. The crisis is deeper than thought

@Prateek, I think this is all speculation at your end. From friends at Amex, no cost-cutting ongoing there, of the scale you indicate. Also, in my prior escalation experiences, Head Customer Services email responds, this is not 2020 but 2016 or so, although there is a team that works under called the Executive Office. Request you to stop posting these theories here unless with proof.

@Prateek

I second with Ajay.

Amex wouldn’t have reopened the Amex Cent/Plat Lounges if they were planning to wrap up/ cut down.

No doubt they have one of the least market capitalisation when it comes to no.of users amongst its peers in India one must understand their business model is more focused towards serving HNIs.

End of the day its a lux travel card.

With massive travel restrictions in place they’re actually loosing more money by giving cash backs.

On a second note, apart from 1 query where I wasn’t happy with the outcome, rest all 100+ queries have been attended & resolved in 12 months.

So, honestly I’m very happy with the services they’re offering.

@Ajay : You’re someone from whom i’ve immensely respected and learnt from since 2014, so i will not proceed before acknowledging how much i appreciate your work over the years, and even going forward.

The response below is with due regard, and is not meant to offend, its an analysis of my thought in relation so unprecedented offers in this crunched WFH era scenario, with some personal experiences referenced.

1) Customer support matrix is a compliance requirement for NBFC’s. Below is an auto-response i received from manager customer services India in September 2020.

From: Manager-CustomerServicesIndia

Date: Fri, 9 Oct 2020 06:11:55 +0000

Subject: Auto Reply

Dear Customer,

Thank you for writing to us.

This is a system-generated response to acknowledge receipt of your e-mail to American Express.

Please allow us to review your email contents and respond back to you within three working days’ time.

Email to manager customer services India on an 25, 2021 at 1:09 AM was answered from head customer services (An L2 responding on L1 email – first thing i noticed – even i use AmEx since 2016).

If emails to L1 are responded by L2, and no response came in committed timelines where did L1 go ? The L1/L2 auto-response mixup never happened before. This is a deal for me, a L1 team missing.

Here are some questions that i have pertaining to their business lately

2) For established brands, Free Cash is typically a way to temporarily boost to sales numbers for given quarter. Most product managers know this. Did anyone see any other well-established bank gives freebies like this, esp in pandemic ?

This year even with extremely low transactions (esp corporate), being majorly a credit payments company, i wonder what compels them to give out over x times worth of offers to customers (They need ~7.8 lac spends on card txns @ 3.5% MDR for recovering the offer amount in this Mega Cashback promo). With more such offers coming in everyday(+merchant denials), how will they recover this money ? No HNI is spending close to what they used to.

Moreover, why and how are such amplified offers are coming (first struck this when 50% cashback on ‘Shop Small’ came in) ? Some NBFC’s do increase volumes to maintain financial ratio’s attractive, but that doesn’t seem to be a point in this case. If they want to retain, just waive off fees. Why spend more of your money instead ? Still can’t find the answer.

With 18% revenue hit and debts almost halved (Q4 2020 vs Q42019), what can be the push to keep giving such strong offers instead of strengthening acceptance (which is the major challenge for Indian market) ? Yes their fees earning increased, but cashbacks worth more are a question for me.

And here is the response for experiences:

3) Chromium browser issue – it took a multiple escalations over June-July 2020 to resolve. This is the resolution provided – AmEx PG page works on Chrome (it sounds illogical, but it is true, i verified it myself on Freecharge on Android) !

4) Small shop merchants in Delhi that denied unless 5% extra

a) Empire stationary mart, nehru place

b) NARANG ELECTRIC CENTRE, kalkaji

Well, these are strictly my opinion, and no bad blood with anyone(including AmEx).

I have never had any ownership of AmEx shares, don’t know anyone at AmEx, just one MRCC (which in my exp has a support system that can only ‘dream’ of matching the issue resolution standards of ANY Citibank team).

I merely analyze NBFC’s for personal interest after the ‘Yes’ fiasco last year. In my view its usually the subtle signs that indicate the problems (first sign: feedback form – never heard such from Citi in almost 8 years since they’re simply brilliant).

@Prateek, remember, Amex works under a special license in India, not NBFC, not full Banking, just a card issuer as a ‘Limited Banking’. The other guys used their income from their cards business to offset other expenses inside the company. Amex, well, cards is the only game they got in India, so it needed to create a moat around its customer base and make sure the high spenders don’t leave, the guys who pay the 3-4% MDR which make Amex do business on its own terms. So, out with the big guns instead of just doing sporadic small offers.

On point 2, Offers that people will remember and be thankful for (like we are!), rather than the chutta 10% off on other products which people may or may not buy. For a product that we pay 60K p.a. for, that justifies it, because even in a bad year, people remember that Amex got their back. Now these big offers could be an aggregation of all the marketing budget of the year. Which means, no sponsorship for a U2 concert this year perhaps, instead this money goes back to the customer in a more tangible form, just Money. Obviously, there would have been modelling done inside the company to compute the lifetime value of the customers who would have been targetted for the offers. And if you think Amex is actually paying 27500 INR for an INR 27500 offer, that definitely is not true. The 5 names would have agreed on a nice discount on the MRPs in exchange for getting this gig. If it is 10% or 25% or some new creative barter, I don’t know. Also, Amex never negotiates on the fee on Platinum Charge Card. This stance has been there for decades. So if they are giving money back, that is cool by them, but the fee is a filter, and that stays. Ask around, you won’t find anyone who got a fee reduction on the Plat Charge or got it free. It is the way they’ve done business. It is the way they want to do business, their call.

On the Shop Small offer, well, on one hand, people complained they gave too less when they were giving 20%, and then there are people complaining they gave too much. Shop Small was a global offer where Amex put 200 million USD on the table, not funded by merchants, but by Amex. It was the first time in India, but it has been going on in the USA for 10 years now or so. This is Amex’s way of getting small merchants to accept Amex, with a carrot, not a stick.

On the expanding acceptance, Amex usually doesn’t discuss price. So unless you don’t show significant volumes, you pay the usual MDR, not a reduced one which is high. Having said that, they have latched on to many more payment networks over the past couple of years, including the SBICard issued terminals and the HDFC issued terminals. An issue that happened late last year, in the holiday season, was a software rollout by one of the payment networks which rendered many machines not accepting Amex until they did a patch. This happened with one of the outlets which was a small merchant and my go-to for many things. They refused Amex one day after accepting it many days, and I tried it on my own with the machine in my hands. So, can’t say it was something that was intentional. As for merchants denying unless 5% extra, since you know about the business so much, you should also know that there is an RBI rule that disallows asking for extra to cover the MDR. You should report the merchants to the issuer and if you paid extra, please do share the proof and they can get them off the network. Here is Kotak commenting on the issue https://www.kotak.com/en/knowledge-centre/why-shouldnt-you-pay-2-at-pos-credit-card-transactions.html You can also dig up the original master circular on the RBI Website. Most of the times we let it fly because, hey, its a small sum and he is the small guy. But if you feel so strongly about it, you should do the right thing and report them to the issuer.

I don’t really understand your Chromium issue so I won’t comment. On Customer Service as well, they are good in my books. I’ve not needed an escalation in years.

One last thing, remember, Amex has created a brand over 170 years giving their high-end customers the wow factor, and then doubled down on it creating the Black. There are enough stories floating about the customer service on the Internet, but here is one or two, https://www.forbes.com/sites/micahsolomon/2017/12/15/american-expresss-customer-service-secrets-consulting-with-amex-on-what-makes-a-difference/?sh=baa6fda40ff3. These episodes are the stuff of legend, and I first read of this many decades ago in a book which I don’t remember now. But they have done this again and again, in markets near and far and made many a surprise happen for customers that I personally know of. The halo effect ends up staying with you, and for Amex customers, they pay the premium fee not just for 1:1 returns on spend, but for the halo of being an Amex cardmember. Of course, there are those who are disappointed and leave as well.

As for the staying power of Amex in India, one bad year (as per you) is nothing that would move an institution. First, in your comments about the offers, you miss the fact that Amex would have made a significant profit over the years which they could have used to make these offers to customers this year. Second, not everyone takes them up on these offers as human psyche is different, and not everyone reads LFAL or cares to ‘maximise’ their card benefits. Let’s call this breakage. Third, if they really were in a bad spot, there is still the global entity to recapitalise them. Here are the Q4 results for Amex global. Mostly a resilient business. https://www.fool.com/earnings/call-transcripts/2021/01/26/american-express-axp-q4-2020-earnings-call-transcr/

I may have jumped over and around and this might come across as disjointed, this is the other side of the story. As for Citi, they haven’t shown any leniency to Prestige members as well, and ask for 20K plus taxes with benefits having been cut down year after year. And in my about 20 years of holding a Citi credit card, I’ve seen enough feedback forms from them as well, and areas where they could have done much much better. Many LFAL readers who swore by the product 5 years ago, might want out now because prestige has thinned out to a shadow of its former self.

now im wondering how do i get that centurion.. only way i can see myself getting marriott platinum

Just take a long staycation at a Cat 1 property. That would be far cheaper and last longer.

Thanks for the info. Received this offer finally.

I have received my card yesterday and there are no offers showing up in my Account’s dashboard. Do I need to do anything to enable these? TIA.

Have not received this offer . In fact my offers section is always empty for my platinum card .

Any thoughts on the monthly fee offer for Platinum Card? I see this option available on my card right now and I’m wondering if this is a good idea instead of going all in for the annual fees to give this a try

Got the email earlier today. With this they’ve given back Rs 60500 across all cash back offers, which is more than what one could have asked for. In effect I have paid just over Rs 10000 for 110000 MR points (had joined via your link), plus all the hotel elite memberships that came with the card. Safe to say they’ve made it almost impossible for me to not renew the card.

Noticed this in my dashboard today. Amex has really pulled out all the stops this year. Nothing like pure cashbacks. The card has already paid for itself (and more) purely through cashbacks. Points earned on spends and other promotions are the bonuses. Its been a great year to be an Amex card holder!

@Lloyd, I’ve been telling people the same thing. They really need to get this card if they haven’t, yet.

Do you think anyone applying now with a referal would get this offer? Or new cardholders will get offers post July26th?

If a product costs more than 27500, can we use it to reduce the price and then pay for it?